![]() Irish Fiscal Advisory Council Strategic Plan 2020–2022

Irish Fiscal Advisory Council Strategic Plan 2020–2022

Introduction

The Fiscal Responsibility Act 2012 established the Irish Fiscal Advisory Council (“the Fiscal Council”) as an independent state body. This is the Fiscal Council’s third strategic plan.

Mission

The Fiscal Council’s mission is to support the effectiveness of fiscal policy in the near and medium-term through delivery on each element of its mandate as an independent fiscal institution.

Vision

The Fiscal Council’s vision is for an economy with broadly based growth in incomes and employment founded on sustainable macroeconomic and fiscal policies.

Values

The key values of the Fiscal Council are:

Background

Mandate of the Fiscal Council

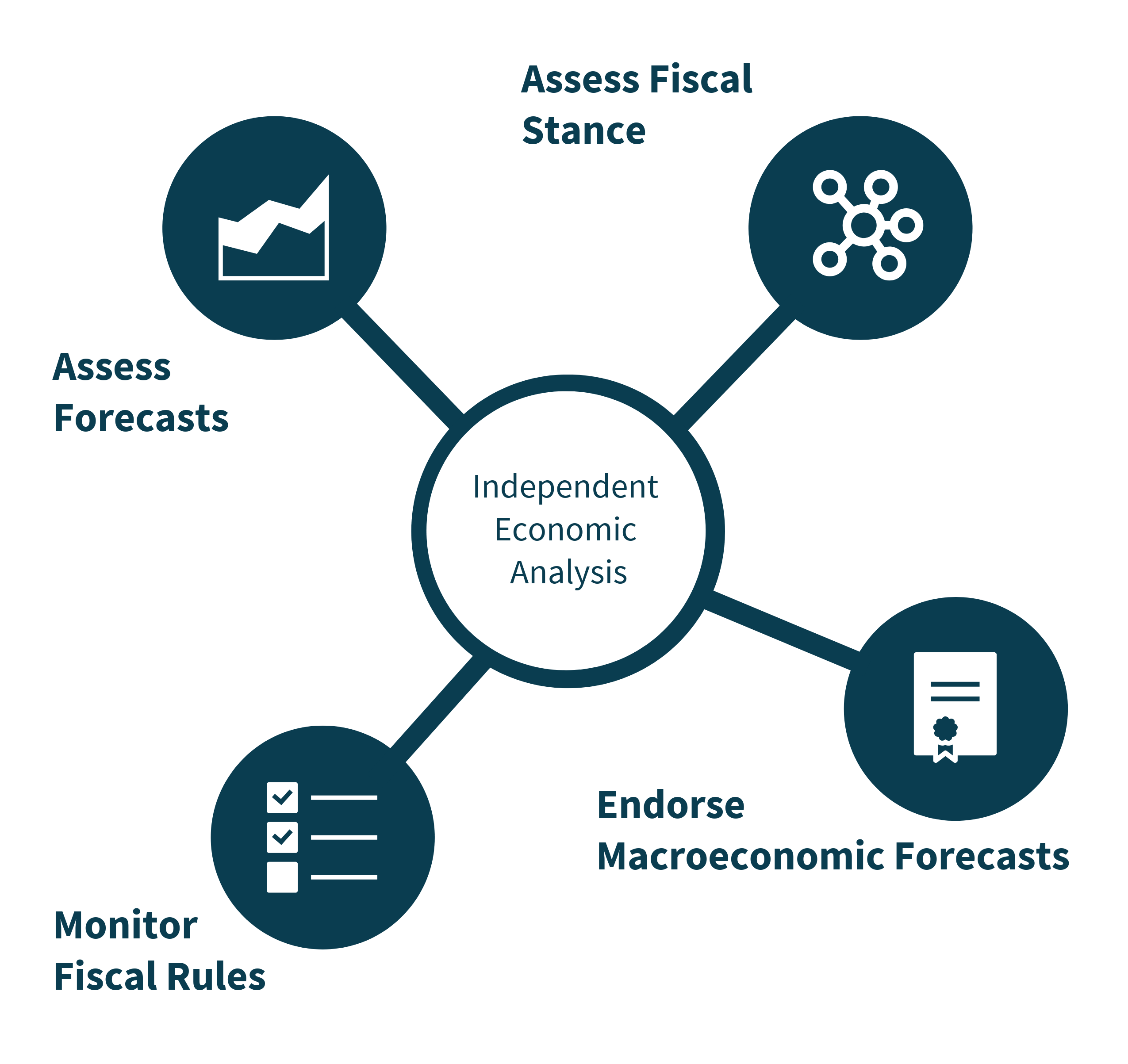

The Fiscal Council has four legally mandated functions. The first three were assigned in the Fiscal Responsibility Act 2012 [1]. The fourth function (endorsement) was assigned to the Fiscal Council in July 2013 [2].

- To assess the official forecasts produced by the Department of Finance and published in the Stability Programme and in the Budget.

- To assess the fiscal stance of Government, and specifically whether it is conducive to prudent economic and budgetary management, with reference to the EU Stability and Growth Pact.

- To monitor and assess compliance with the Budgetary Rule [3].

- To endorse the official macroeconomic forecasts prepared by the Department of Finance in relation to each Budget and Stability Programme. This follows revised European requirements to have national medium-term fiscal plans and draft budgets based on independent macroeconomic forecasts, which means macroeconomic forecasts produced or endorsed by an independent body. A joint Memorandum of Understanding between the Fiscal Council and the Department of Finance underpins the endorsement process [4].

The Fiscal Council produces biannual Fiscal Assessment Reports as well as an annual Pre-Budget Statement. Reports are submitted to the Minister for Finance and subsequently published within ten days. The Fiscal Council also submits its Annual Report to the Minister who arranges to lay the Report before each House of the Oireachtas. The Council chairperson may also be required to appear before the Oireachtas in relation to its activities.

The Fiscal Council produces biannual Fiscal Assessment Reports, as well as an annual Pre-Budget Statement. Reports are submitted to the Minister for Finance and subsequently published within ten days. The Fiscal Council also submits its Annual Report to the Minister who arranges to lay the Report before each House of the Oireachtas. The Council chairperson may also be required to appear before the Oireachtas in relation to its activities.

In relation to the endorsement function, the Council is required to provide a formal letter to the Secretary General of the Department of Finance at least five working days before the Department publishes the Budget and Stability Programme [5]. If the Council were to conclude that it had significant reservations about the preliminary or “provisional final” macroeconomic forecasts, it would immediately communicate these informally to the Department. If, following further discussions, the Council were still not in a position to endorse the macroeconomic forecasts underlying the Budget or SPU, the Chair would write to the Secretary General explaining why this was the case, at least five working days before the Department publishes the Budget or SPU.

To support the Fiscal Council’s delivery of its mandate, the Council also produces ad hoc reports including Analytical Notes, Working Papers and other analytical work on the Irish economy, macroeconomic forecasting, and fiscal policy, in addition to an annual Ex-Post Assessment of Compliance with the Domestic Budgetary Rule.

Current Position of the Council and Progress to Date

The Minister for Finance appointed the Council’s five members based on their experience and competence in domestic and international macroeconomic and fiscal matters. The current Council has a strong international dimension with two members based outside of Ireland.

The Secretariat comprises of a Chief Economist, two Economists, three Research Assistants, and an Administrator.

To date, the Council has published:

17 Fiscal Assessment Reports

- October 2011

- April 2012

- September 2012

- April 2013

- November 2013

- June 2014

- November 2014

- June 2015

- November 2015

- June 2016

- November 2016

- June 2017

- November 2017

- June 2018

- November 2018

- June 2019

- November 2019

6 Pre-Budget Statements

- Budget 2015

- Budget 2016

- Budget 2017

- Budget 2018

- Budget 2019

13 Endorsement Letters

- October 2013

- April 2014

- October 2014

- March 2015

- October 2015

- April 2016

- October 2016

- April 2017

- September 2017

- April 2018

- October 2018

- April 2019

- September 2019

1 Ex-Post Assessment of Compliance with the Domestic Budgetary Rule

- 2016

12 Analytical Notes

- “House Price Risks”

- “Sensitivity Analysis of the Department of Finance Approach to Potential Output Estimation under the EC Methodology”

- “Tax Forecasting Error Decomposition”

- “DIRT Forecast Methodology”

- “Future Implications of the Debt Rule”

- “Adoption of New International Standards for National Accounts and Balance of Payments”

- “The EU Expenditure Benchmark: Operational Issues for Ireland in 2016”

- “Controlling the Health Budget: Annual Budget Implementation in the Public Health Area”

- “Public Capital: Investment Stocks and Depreciation”

- “Challenges Forecasting Irish Corporation Tax”

- “A “Heat Map” for Monitoring Imbalances in the Irish Economy”

- “Estimating Ireland’s Budgetary Semi-Elasticities”

11 Working Papers

- “Strengthening Ireland’s Fiscal Institutions” (January 2012)

- “The Government’s Balance Sheet after the Crisis: A Comprehensive Perspective” (September 2013)

- “Uncertainty in Macroeconomic Data: The Case of Ireland” (March 2015)

- “An Analysis of Tax Forecasting Errors in Ireland” (September 2015)

- “Producing Short-Term Forecasts of the Irish Economy” (May 2017)

- “Estimating Ireland’s Output Gap” (January 2018)

- “Designing a Rainy Day Fund to Work Within the Fiscal Rules” (June 2018)

- “Nowcasting to Predict Data Revisions” (October 2018)

- “Ireland’s spending Multipliers” (January 2019)

- “The Current Account, a Real-Time Signal of Economic Imbalances or 20/20 Hindsight?” (March 2019)

- “Estimating Ireland’s Tax Elasticities: A Policy-Adjusted Approach” (June 2019)

1 Independent Review of the Irish Fiscal Advisory Council

- June 2015

Key Challenges, Risks and Opportunities in our Operating Environment

Key Challenges

- Visibility: The Fiscal Council needs to ensure awareness of its mandate and assessments, which cover key government decisions, in a crowded field of public debate, while ensuring that credibility is maintained.

- Administrative burden: Achieving all elements of its mandate and expanding on Fiscal Council’s analytical output is a challenge, given the small size of the Secretariat. Progress in relation to the development of more robust analysis of long-term fiscal projections and of fiscal risks is a resource-intensive process.

- Data/informational asymmetries: Government departments and bodies may have relevant information that cannot be accessed for Fiscal Council analysis.

- Difficulties with interpretation of Irish national accounts: Some difficulties remain with the interpretation of Irish national accounts, and the link between measures and rules, which can be a challenge.

- Capacity: The Fiscal Council’s resources are small and declining. Its ceiling is linked to the Harmonised Index of Consumer Prices. Given that this tends to rise at a slower pace than wages-the Fiscal Council’s main item of expenditure-this will constraint the Fiscal Council’s ability to sustain current output into the future and to respond to changing circumstances or new analytical requirements.

Risks

- Small size of Secretariat: The Fiscal Council is at risk if staff were to suddenly leave or to take periods of extended absence as there is limited scope for duplication of skill sets resulting in reliance on key personnel.

- Impact: Changing economic fortunes, political changes, or developments in the EU and Irish institutional framework could limit the ability of the Fiscal Council to contribute to prudent and sustainable fiscal policy.

- Independence: Although the Fiscal Council’s independence is underpinned by legislation, there could be moves to reduce current protections in the future.

- Cooperation: The Fiscal Council is highly reliant on information from government departments and agencies, which is provided by goodwill rather than formal information-sharing arrangements. If this goodwill were to diminish, access to information could become more constrained.

- Conflict with Government: The Fiscal Council may be required to risk controversy by publishing criticisms of Government policy or unwelcome advice where the Council considers that it is warranted. This is in line with its independent role and mandate.

- Organisational risks: Disruption to existing service-level agreements could severely impede the functioning of the Council.

- Conflicts arising between the technical application of the fiscal rules and overall recommendations on the fiscal stance: Following Ireland’s exit from the EU-IMF programme of financial support on 15th of December 2013 and its achievement of a deficit below 3 per cent of GDP in 2015, it entered into the Preventive Arm of the Stability and Growth Pact. This has given more importance to the new budgetary framework, comprising greater surveillance (including that of the Fiscal Council) and a system of domestic and EU fiscal rules. However, there are several features of how the fiscal rules are applied that are not working well at present, including a tendency to exhibit procyclicality (Casey et al., 2018; Barnes and Casey, 2019). There is a risk that the Fiscal Council’s assessments—which reflect its assessment of the broader fiscal stance and which draw on the Council’s “principles-based approach to the fiscal rules”—might conflict with European Commission’s assessments of the rules. This could weaken the credibility of the fiscal framework or lessen the impact of the Fiscal Council’s assessments.

Opportunities

- Deeper analysis/research: A larger Secretariat gives scope for richer analysis, for making output more visible to relevant public bodies and the general public, for continuing to build the Fiscal Council’s reputation, and for developing long-term analysis of the public finances.

- European and domestic agenda: The Fiscal Council could have a greater role in the European and domestic debate on fiscal rules, structures, and economic governance including through its participation in the OECD/EU IFI Network(s).

Strategic Goals

Central Goal: Deliver on all Elements of our Mandate

| Goal | Outputs |

|---|---|

Assessment of:

|

The Fiscal Council will:

|

| Endorsement of Macroeconomic Forecasts. |

|

Supporting Goal 1: Ensure Compliance with all Requirements for a Statutory Body

| Goal | Outputs |

|---|---|

| Publication of Annual report and a set of financial accounts. | The Fiscal Council will:

|

| Independence and transparency. |

|

| External review of Fiscal Council operations. |

|

Supporting Goal 2: Promote Awareness of Fiscal Policy issues

| Goal | Outputs |

|---|---|

| Two Fiscal Assessment Reports and a Pre-Budget Statement every year |

|

| Analytical Notes and Working Papers |

|

| External communications and awareness of the Fiscal Council |

|

Achieving Our Goals

| Goal | Outputs |

|---|---|

Economic Forecasting:

|

|

| Public Finances. |

|

| Fiscal Rules. |

|

| Full-time seven-person Secretariat. |

|

| Stakeholders. |

|