26 June 2026 – Beyond the Budget Series

Brian Cronin, Economist

We know foreign-owned multinationals in Ireland pay the bulk of Ireland’s corporation tax receipts: in 2025, they paid 87% of them (Gannon et al, 2026).

But Ireland’s reliance on these firms extends far beyond corporation tax. These companies also contribute to the Exchequer in other ways. As major employers, they provide high paying jobs, which result in substantial payroll taxes and social contributions. Their spending on goods and services also generates sizable VAT receipts.

In this blog, we focus on the three key sectors that underpin Ireland’s foreign direct investment model: manufacturing, tech, and financial services. Since 2020, these sectors have been the top-three biggest corporation taxpayers.

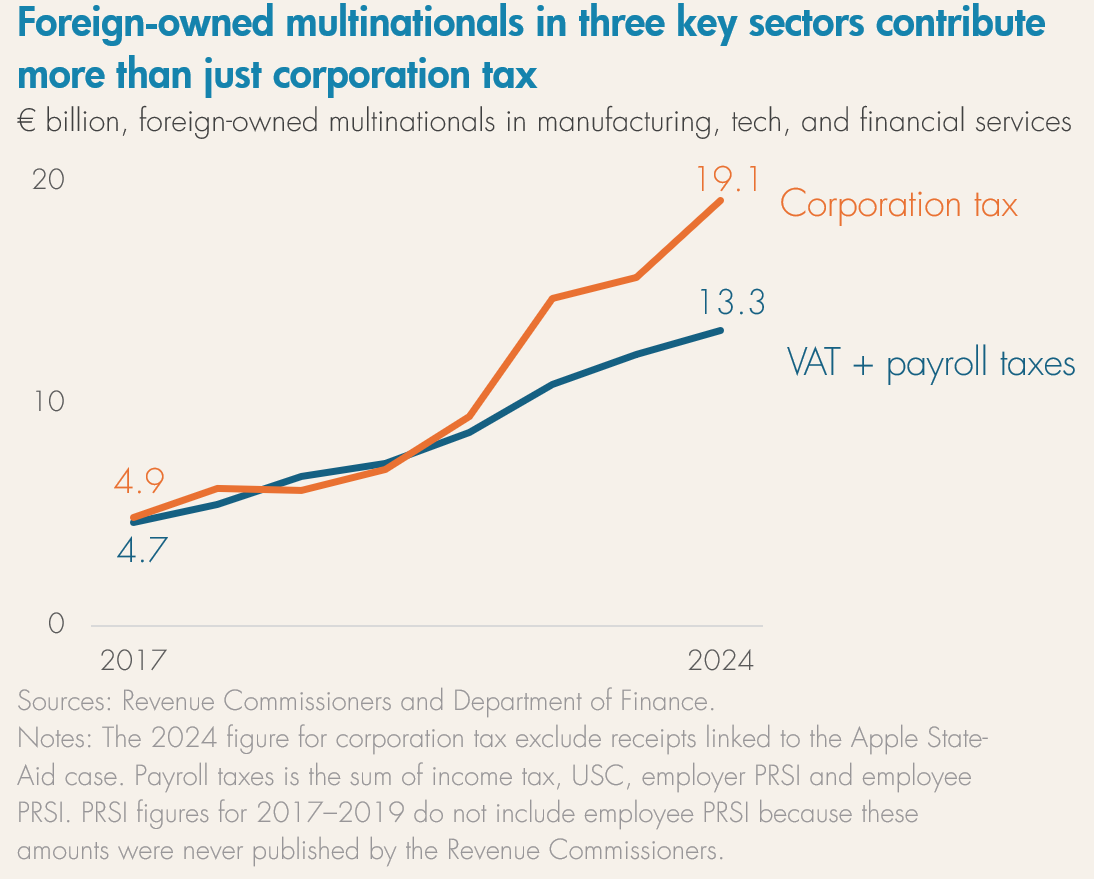

In 2024, foreign-owned multinationals in these three sectors paid over €19 billion in corporation tax. This accounted for almost 70% of total corporation tax.1 That same year, these firms also contributed over €13 billion in payroll taxes and VAT — more than the Government spent on housing and transport combined.2

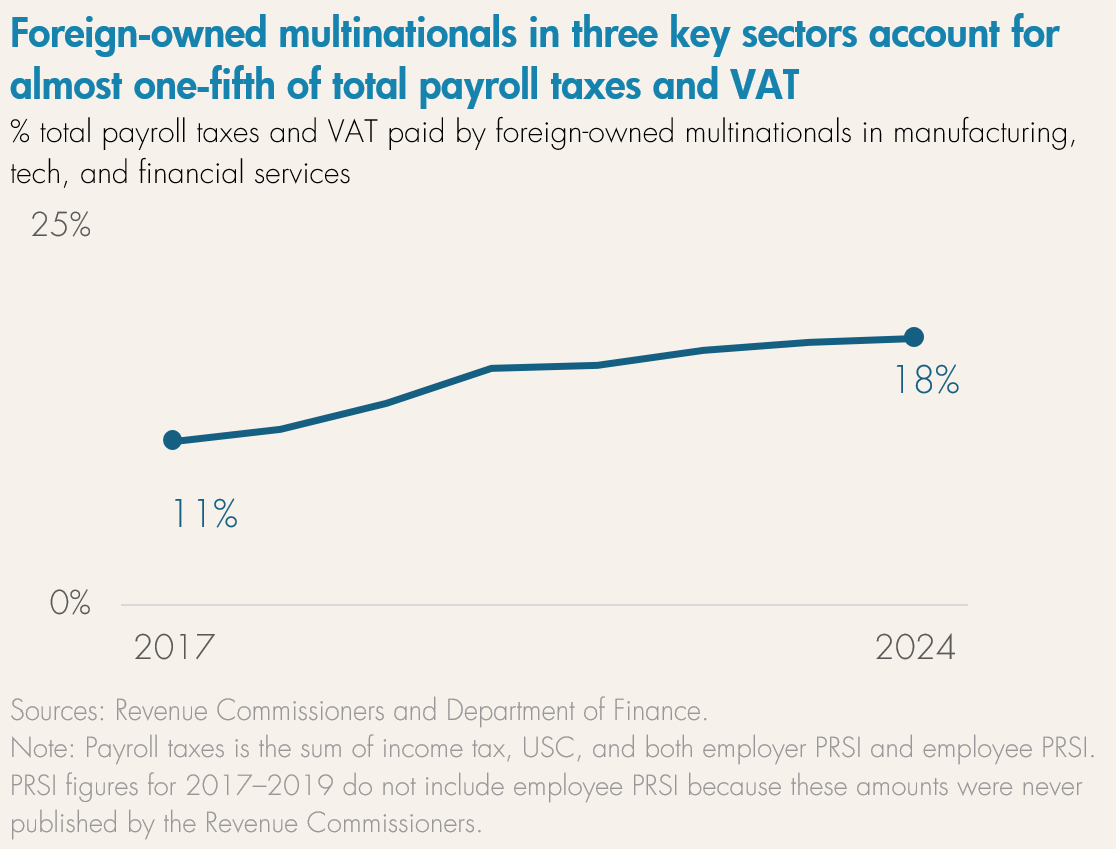

This reliance on foreign-owned firms in three key sectors has also grown over time. In 2017, these firms accounted for 11% of the total payroll taxes and VAT collected. By 2024, this share had reached 18%.3 In other words, almost €1 out of every €5 collected in income tax, USC, PRSI, and VAT comes from foreign-owned firms in manufacturing, tech and financial services.

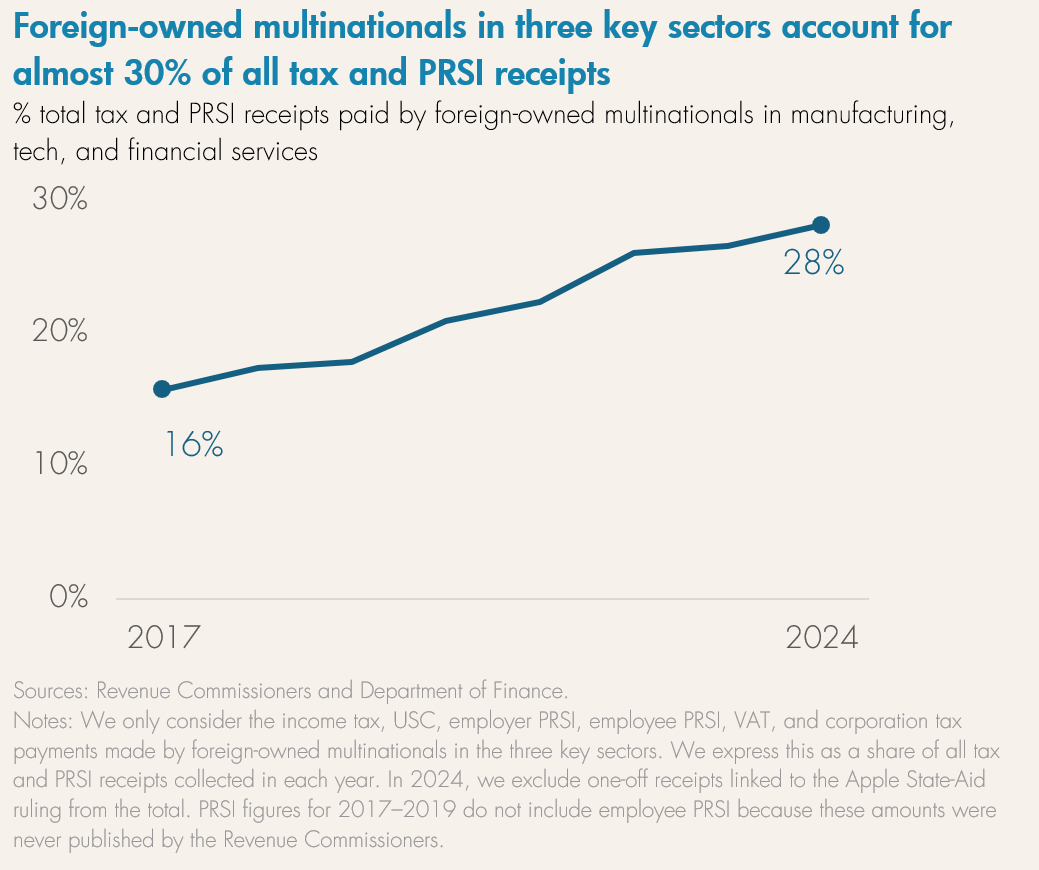

The scale of the State’s growing reliance on these foreign-owned firms becomes even clearer when we add the corporation tax they pay to their VAT and payroll tax payments. In 2017, foreign-owned multinationals in manufacturing, tech, and financial services accounted for 16% of all tax and PRSI receipts. By 2024, that figure had almost doubled to 28%.4 In other words, almost €3 in every €10 collected by the State in tax and PRSI now comes from foreign-owned multinationals operating in these three sectors.

The top ten corporation taxpayers provide highly paid and highly taxed jobs

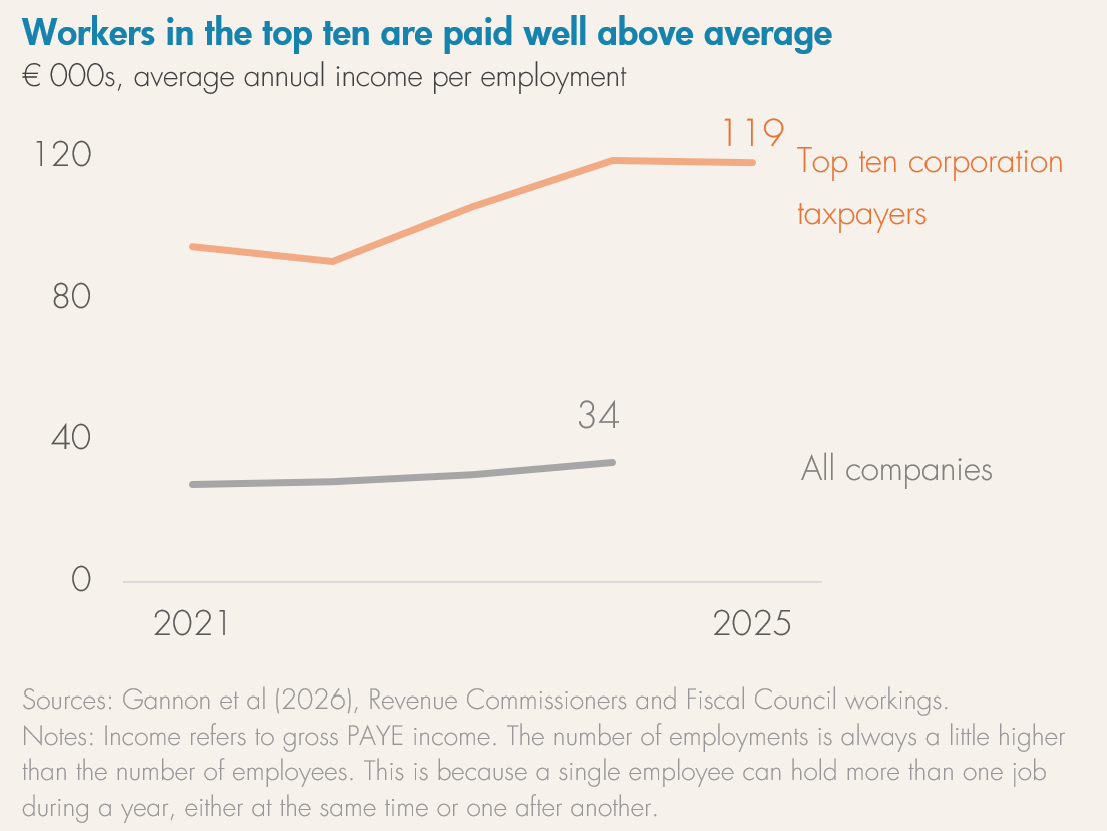

Since 2021, the Revenue Commissioners have published data on the payroll taxes paid by employees working for the top ten corporate taxpayers. While the composition of the top ten may change, these companies are typically large employers. Employment in these firms has stayed fairly steady, averaging around 39,000.5

Workers in the top ten corporation taxpayers are paid well above average. In 2025, the average annual income per employment was €119,000, more than three times greater than the national average (Gannon et al, 2026).6

Payroll taxes amount to around 45% of employment income in the top ten corporation taxpayers. This is much higher than the national average of 36%. In 2025, the top ten corporation taxpayers paid €2.3 billion in payroll taxes (Gannon et al, 2026). This amounts to about 4% of the national total, or €1 in every €25 collected.7

What would this mean for a single multinational? Consider a hypothetical large multinational operating in the tech sector.8 Drawing on representative firms, the cost of wages, salaries, and share-based pay could amount to around €160,000 per direct employee. This could entail tax revenues for an average employee of around €65,000 when considering income tax, employees’ PRSI, and the USC.9 Adding employers’ PRSI, total payroll taxes could amount to around €80,000.10

If the firm were to employ say 6,500 workers in Ireland, that would entail a payroll-related tax bill of about €500 million. These estimates do not account for the knock-on impacts on other firms whose business models may depend heavily on the presence of these multinationals (Brady, 2019).11

VAT and payroll-related taxes are likely to be less risky

The payroll taxes and VAT associated with foreign multinationals in Ireland are likely to be less volatile than the corporation tax they pay. Many of these firms have made substantial long-term investments in Ireland over several decades. In the manufacturing sector, in particular, physical investments in plants would not be easily moved to another jurisdiction. Ireland is often deeply embedded in their global business models, serving as a base for sales across the EU and other international markets.

These firms are unlikely to significantly scale back activities in Ireland in the short term. But the long-term downside risks are clear. Multinationals could restructure their activities and gradually reduce their footprint in Ireland. And artificial intelligence could displace some high-paying jobs (Doorley et al, 2026).12

One way to mitigate these risks is to continue to make Ireland an attractive location for investment. Ireland’s infrastructure shortcomings are frequently cited as a major concern for large employers (EY, 2026; IBEC, 2026; American Chamber of Commerce Ireland, 2025). Given known shortages in housing, water, energy and transport infrastructure (Conroy and Timoney, 2024), there is a clear case for public investment to help resolve these issues. This could not only support existing employers but also improve Ireland’s ability to attract new investment.

The opinions expressed and arguments employed in these blogs do not necessarily reflect the official views of the Fiscal Council.

Footnotes

- This is after we exclude one-off receipts linked to the Apple State-Aid ruling. ↩︎

- Payroll taxes is the sum of income tax, USC, and both Employer PRSI and Employee PRSI. ↩︎

- Foreign-owned multinationals in manufacturing, tech, and financial services accounted for around 10% of all employments in 2024 (Gannon et al, 2026; Duke et al, 2026). ↩︎

- Total tax receipts amounted to €97.1 billion in 2024, excluding the one-off receipts linked to the Apple State-Aid ruling. The largest sources of tax revenue were income tax (€35.1 billion), corporation tax (€28.1 billion), VAT (€21.8 billion) and excise duty (€6.3 billion). Total PRSI receipts amounted to a further €18.1 billion. ↩︎

- The number of employments is always a bit higher than the number of employees. This is because a single employee can hold more than one job in a given year, either at the same time or one after another (Collins et al, 2024). Nevertheless, employments provide a useful estimate of the number of employees. ↩︎

- Here, income refers to gross PAYE employment income. It includes all wages and salaries, bonuses, and share-based pay. It is the employee’s pay before any pension contributions or salary sacrifice deductions are made (Revenue Commissioners, 2026). ↩︎

- This share has remained fairly steady since data was first published by Revenue in 2021. ↩︎

- The figures provided are not specific to any one multinational firm. Rather, they are representative of a number of firms operating in the tech sector in Ireland and are based on data included in their annual financial statements. These firms are likely to be among Ireland’s biggest corporation taxpayers. ↩︎

- This estimate is for a single person with gross income of €160,000. Income tax, employees’ PRSI, and USC amounts were estimated with an income tax calculator. ↩︎

- Our employers’ PRSI estimate is based on the figures included in company financial statements. ↩︎

- These estimates also exclude the VAT employees pay when they spend their income. ↩︎

- There are also potential upside risks. Despite growing global competition for foreign direct investment, Ireland is likely to remain an attractive location due to its relatively stable business environment, skilled English-speaking workforce, access to international markets, and competitive corporate tax regime. If Ireland manages the skills transition effectively, it could be a net beneficiary of the technological changes brought about by artificial intelligence. ↩︎